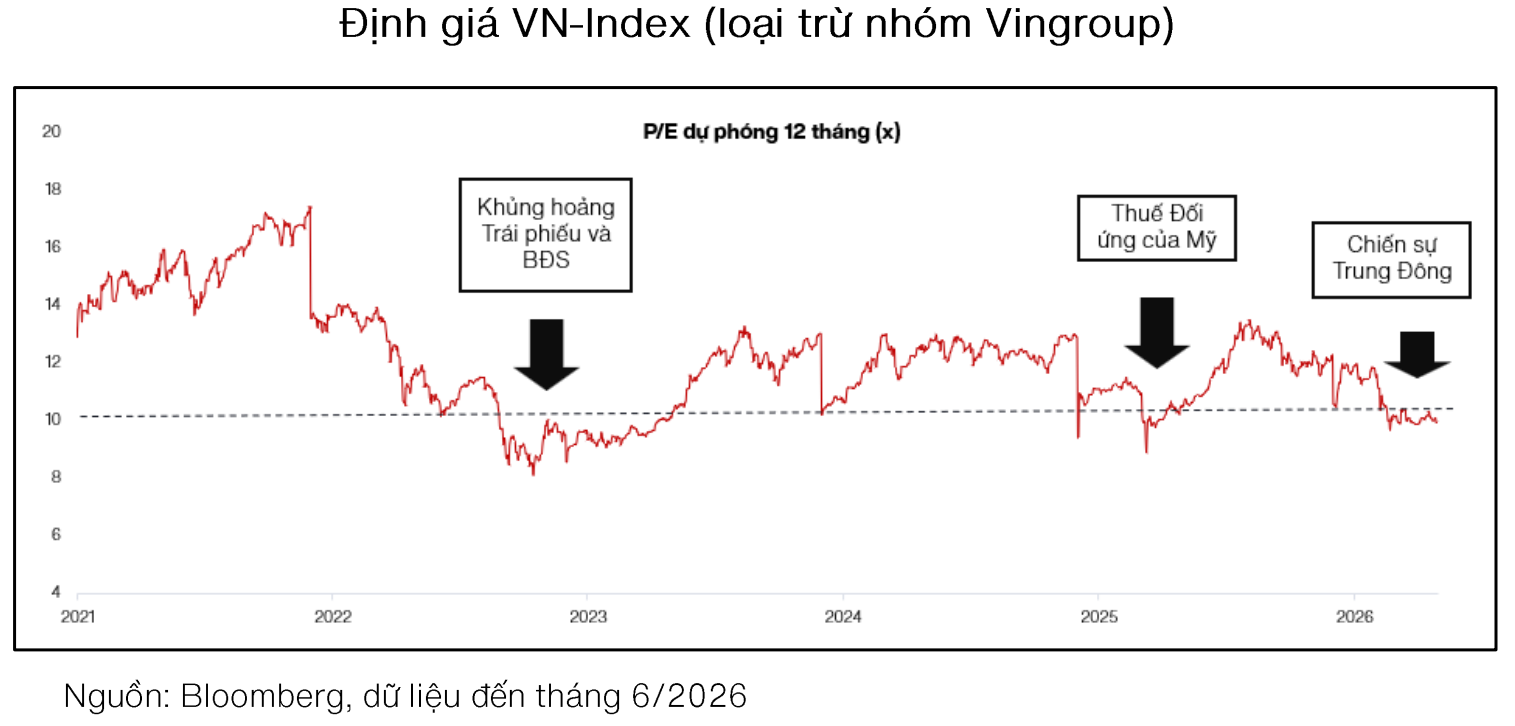

VinaCapital presented this assessment in its market valuation report released on 4/6. The fund noted that the VN-Index is currently trading at a price-to-earnings (P/E) ratio of approximately 13, while profit growth for this year is anticipated to reach 15%. Viewed solely through the overall index, this valuation does not appear exceptionally low.

"However, over 70% of stocks in the market are trading below a P/E ratio of 10, a range usually observed only during crisis periods," VinaCapital's report stated. The firm attributed this to the strong rally in stocks within the Vingroup ecosystem, which accounts for nearly 30% of the VN-Index's capitalization, making the remaining market appear cheaper relative to the overall index.

VinaCapital's analysis department believes that the widespread low valuation across most of the market completely contradicts current realities. Vietnam's economy continues to demonstrate strong resilience, and technology exports are experiencing robust growth.

|

VN-Index P/E from 2021 to present. Data: VinaCapital. |

Beyond valuation, the profit growth momentum of businesses is also considered a bright spot by the fund. In Q1, after-tax profits of listed companies improved by 51% year-on-year, significantly surpassing market expectations of 15%.

Excluding the exceptional performance of Vinhomes, overall market profit still increased by approximately 30%, double investor expectations. This indicates that businesses possess strong fundamental foundations, even as the US-Iran conflict heavily impacts the global economy. This growth momentum is also evident across numerous sectors, including: real estate, materials, retail, energy, and essential consumer goods.

Another point highlighted by VinaCapital in its report is that Vietnamese securities have not yet fully reflected the impact of ongoing reforms. These factors encompass enhancing the operational efficiency of state-owned enterprises, the potential to meet criteria for market upgrade, and policies aimed at resolving stalled real estate projects.

VinaCapital assesses that these changes may not immediately affect stock prices. Nevertheless, the new policies will gradually materialize through improved liquidity and an increased number of listed companies.

From a capital market perspective, this information is crucial amid continued net selling by foreign investors. Year-to-date, foreign investors have recorded net sales in 15 sessions. Specifically, net selling on 4/6 amounted to approximately 5,775 billion VND.

While foreign capital outflow poses a challenge, it is not the sole variable influencing the outlook for Vietnamese securities, according to VinaCapital. If liquidity improves, the market upgrade process progresses, and the supply of new listed companies increases, the current low valuation landscape could be viewed differently.

|

Stock trading at Kafi exchange. Photo: Quynh Tran |

Alongside favorable conditions, VinaCapital also identified several macroeconomic challenges for Vietnamese securities, such as: transport disruptions in the Strait of Hormuz, a widening trade deficit, and inflation risks.

According to data from the General Statistics Office (Ministry of Finance), in the first five months of the year, Vietnam's total merchandise import-export turnover reached over 445 billion USD, marking a 25% increase compared to the same period last year. After ten consecutive years of trade surplus (2016-2025), Vietnam's merchandise trade balance shifted to a deficit of 13.8 billion USD in the first five months of the year.

Concurrently, VinaCapital noted that Vietnam's trade deficit (import surplus) increased from approximately 3% of GDP to over 6% of GDP by mid-May, equivalent to about 13 billion USD. The fund attributes over two percentage points of this increase to the Middle East conflict, due to sharp rises in oil prices and the Chinese yuan.

However, the majority of Vietnam's import surplus stems from increased purchases of raw materials and production inputs serving high-tech industries. VinaCapital considers this a significant point, explaining why the currency and stock markets are somewhat less concerned about the imbalance in the trade balance.

Trong Hieu