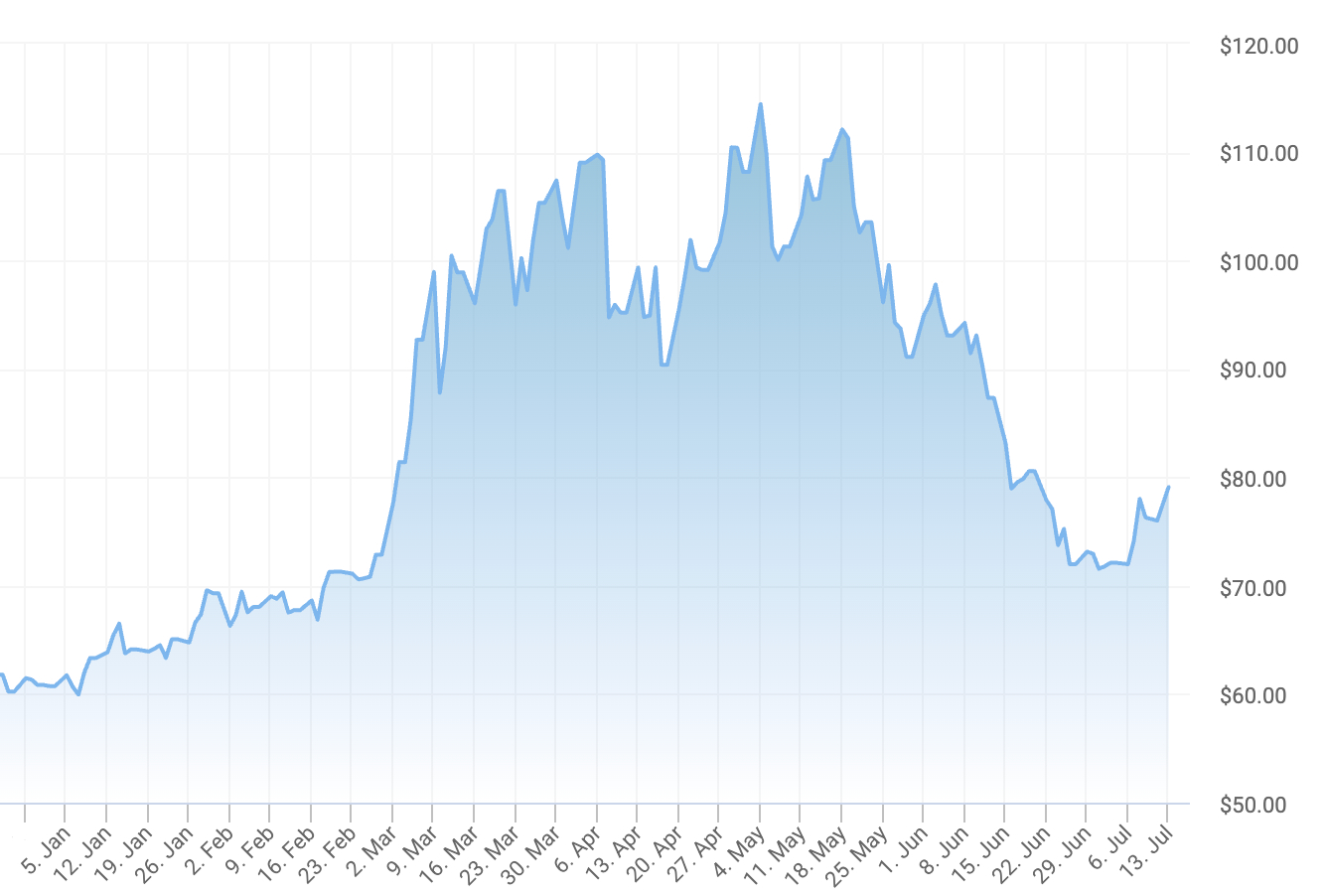

Opening on 13/7, both Brent and WTI crude oil prices rose by nearly 4%. A barrel of Brent cost 78,7 USD, while WTI was 74 USD. The market moved upward as conflict in the Middle East escalated again last weekend.

However, even with tensions between the U.S. and Iran escalating again earlier this month, oil prices did not surge. In contrast, in May, oil prices at one point exceeded 110 USD per barrel.

Explaining this, Jim Burkhard, Vice President and Head of Crude Oil Research at S&P Global Energy, assessed that grey zone conflict – primarily naval confrontations between the U.S. and Iran – no longer shocks the market.

"It can cause oil prices to rise or fall by a few USD, as happened a few days ago, but it is not a shock like earlier in March, when Iran did something many had never thought possible (completely blockading the Strait of Hormuz)," he said.

|

Brent crude oil price movements (USD/barrel) year-to-date. *Source: OilPrice* |

Meanwhile, oil production from the Middle East to the world has improved through various means. According to AP, oil exports from the Gulf region, including those passing through the Strait of Hormuz and other alternative routes, have reached approximately 14 million barrels per day. Although still lower than the pre-war level of 20 million barrels, this marks a significant increase compared to the peak of the conflict.

Tamas Varga, an analyst at PVM Oil Associates, also believes the market has adapted effectively. According to his calculations, Gulf countries have utilized alternative export routes and covert shipments to reduce the actual deficit to approximately 12,2 million barrels per day.

Concurrently, non-Gulf producers have increased output, and the U.S. has released strategic reserves and granted sanctions waivers for Russian and Iranian oil. These measures have added an extra 9,1 million barrels, bringing the actual deficit down to only about 3,1 million barrels per day.

Notably, global consumption is decreasing. "A large amount of crude oil is being released into the market, but demand for it is lower," said Jim Burkhard. The main reason is that the Asian market, a region highly dependent on Middle Eastern oil sources, is buying significantly less.

Among them, China is leading the reduction. According to Burkhard, the country decided to sharply cut oil purchases from the international market when prices rose in the spring, causing consumption to decrease by nearly 6 million barrels per day.

ING Bank (Netherlands) reported that crude oil imports by the world's second-largest economy in May decreased by 30% compared to the same period in 2025. Vessel tracking data indicates June imports have decreased even further. "The biggest uncertainty for the market is when China will resume buying oil. Their prolonged absence could put pressure on prices," the ING team noted.

According to Daniel Sternoff, a senior research fellow at the Center on Global Energy Policy at Columbia University, China has had additional incentives to conserve fuel for road transport and increase the use of electric vehicles recently.

"Based on what we have observed since the crisis began, China's demand for gasoline and diesel is estimated to have decreased by about 500,000 to 600,000 barrels per day. This is a very significant figure," Sternoff noted.

According to forecasts from the International Energy Agency (IEA), global oil demand will decline for the first time since the 2020 pandemic, by one million barrels per day. Toril Bosoni, Head of Oil Markets and Industry at the IEA, stated that the market could return to a surplus state as early as the end of this year, due to a significant increase in production from non-Gulf producers and lower-than-expected demand.

"This significantly reduces pressure on the market and allows countries to rebuild reserves," she said. However, the IEA also noted that the forecast for a surplus by the end of this year depends on the assumption that oil tanker traffic through the strait will gradually recover, allowing producers to restart fields and refineries. Toril Bosoni acknowledged there will be no "quick or linear" recovery because "the situation is very uncertain and unstable."

Assuming no further significant disruptions to the flow through the Strait of Hormuz, ING forecasts average Brent oil prices at 80 USD per barrel in QIII and 74 USD per barrel in QIV.

Jim Burkhard at S&P Global Energy noted that the struggle for control of the strait between the U.S. and Iran is not yet over, making a full restoration of maritime traffic through Hormuz unlikely. "The future of the Strait of Hormuz is perhaps even more uncertain now than when the conflict began," he commented.

By Phien An (according to AP, CNBC, ING)